Local Market Snapshot: June 2026 in the Longleaf Pine REALTORS® Region

What REALTORS® Are Seeing Across Our Communities Last Month

June housing data across the Longleaf Pine REALTORS® region reflects a market with more available inventory, stronger contract and closing activity, and continued price growth—alongside a slower, more deliberate pace for many buyers and sellers.

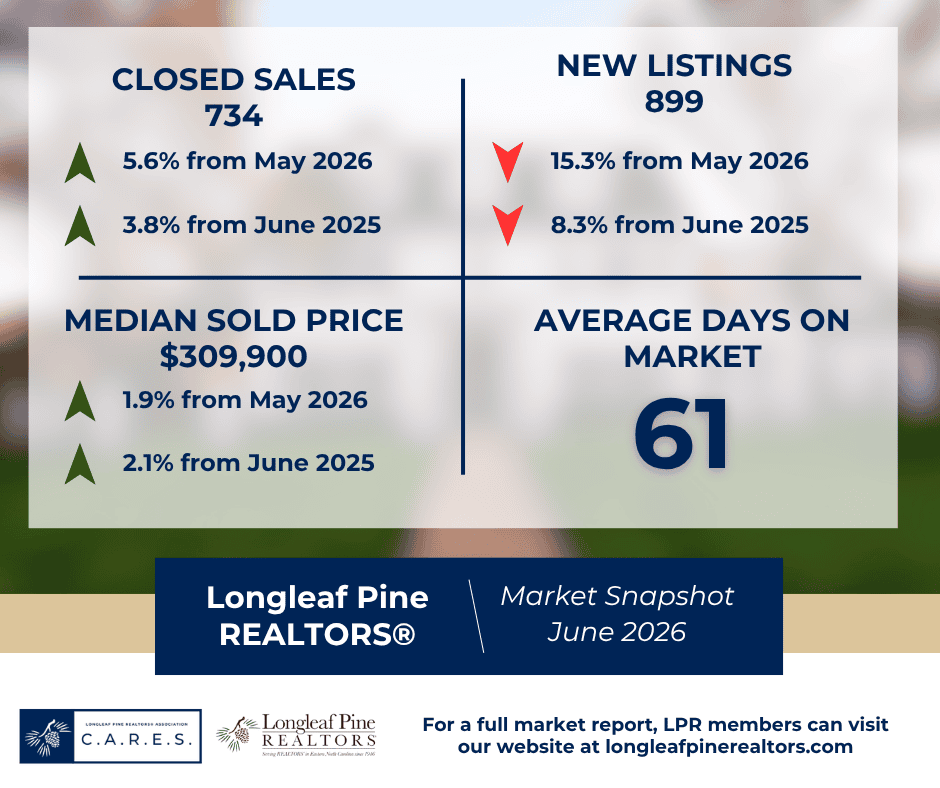

Across all residential properties, new listings declined 8.3 percent year over year to 899. Pending sales increased 6.6 percent to 707, while closed sales rose 3.8 percent to 734. Homes for sale increased 10.5 percent to 2,535, bringing the region to 4.1 months of inventory. The median sales price increased 2.1 percent to $309,900, while the average sales price rose 1.4 percent to $319,904.

The year-to-date picture remains steady. Through June, new listings were up 0.8 percent, pending sales increased 2.3 percent, and closed sales rose 0.5 percent compared with the same period last year. The year-to-date median sales price increased 0.3 percent to $299,900, while the average sales price rose 1.3 percent to $310,218.

The broader rolling 12-month view shows continued activity at higher price points. From July 2025 through June 2026, pending sales increased 1.0 percent overall. The $350,000-and-above range posted the strongest gain, rising 6.5 percent, while new-construction pending sales increased 3.1 percent. The rolling median sales price rose 2.7 percent to $299,000, with townhouse and condo properties recording the strongest price growth at 16.8 percent to $198,000.

Regional Overview

June’s numbers point to a market that remains active while continuing its transition toward more balanced conditions. Buyers have more choices than they did a year ago, but properties are also taking longer to move from listing to accepted offer. Days on market across all residential properties increased 15.1 percent to 61 days, while sellers received an average of 98.7 percent of their most recent list price.

That combination reinforces the importance of accurate pricing, thoughtful preparation, and a strong marketing strategy. Buyers remain engaged, but they have more time and inventory to compare before making a decision.

Existing Single-Family Homes

Existing single-family homes remained the largest source of regional activity. New listings increased slightly, rising 0.7 percent to 733, while pending sales jumped 13.2 percent to 532. Closed sales were nearly unchanged at 511, up 0.2 percent year over year.

Inventory increased 10.0 percent to 1,595 homes, while months of supply rose from 3.3 to 3.6. The median sales price increased 1.8 percent to $290,000, and the average sales price rose 0.7 percent to $309,738. Days on market increased from 36 to 42 days, indicating that this segment remains active but is moving at a more measured pace.

New Construction

New construction continued to provide a significant share of available inventory. Closed sales increased 9.4 percent to 187, despite a 38.5 percent decline in new listings and a 4.1 percent decrease in pending sales.

Inventory rose 11.3 percent to 780 homes, producing 5.0 months of supply. The median new-construction sales price increased 1.6 percent to $348,323, while the average price rose 2.6 percent to $369,093. New-construction homes received an average of 99.8 percent of list price and spent 104 days on the market.

The segment continues to offer buyers additional choices, particularly for those comparing incentives, financing options, move-in timelines, and available resale inventory.

Townhouses and Condominiums

Townhouse and condo activity produced mixed results in June. New listings declined 19.3 percent to 46, and pending sales fell 26.7 percent to 33. Closed sales, however, increased 38.5 percent to 36.

Inventory rose 11.1 percent to 160 properties, with 5.4 months of supply. The monthly median sales price increased sharply to $242,000, while the average sales price rose 14.5 percent to $206,050. Because this is a smaller segment with fewer monthly transactions, individual sales can have a greater effect on percentage changes. The rolling 12-month median of $198,000, up 16.8 percent, provides additional evidence of longer-term price growth in this property type.

County-by-County Snapshot

Cumberland County

Cumberland County recorded 5,162 showings in June, up 5.8 percent year over year but down 9.2 percent from May. Buyer interest increased 14.1 percent from a year ago to 3.8 showings per listing, while managed listings declined 7.3 percent to 1,431.

The $150,000-to-$249,999 range generated the most activity with 2,071 showings and the strongest buyer interest at 4.5 showings per listing. The $250,000-to-$349,999 range followed with 1,631 showings, while homes priced at $350,000 and above recorded 964 showings. Cumberland’s data reflects broad demand, with the strongest engagement continuing in attainable and mid-market price ranges.

Hoke County

Hoke County recorded 852 showings in June, down 11.1 percent year over year and 11.2 percent from May. Buyer interest measured 3.2 showings per listing, while managed listings declined to 310.

The $250,000-to-$349,999 range led the county with 483 showings, followed by the $350,000-and-above range with 216. The $150,000-to-$249,999 segment generated 145 showings and the strongest buyer interest among the county’s primary price ranges at 4.8 showings per listing. Although overall showing activity declined, interest remained concentrated in Hoke County’s attainable and mid-market inventory.

Lee County

Lee County recorded 412 showings in June, an increase of 26.4 percent year over year and 11.7 percent from May. Buyer interest measured 3.5 showings per listing, while managed listings rose 31.4 percent to 134.

The $350,000-and-above range generated the most activity with 175 showings, followed by the $250,000-to-$349,999 range with 146. More affordable homes remained especially competitive when available: properties priced below $150,000 averaged 8.0 showings per listing, while the $150,000-to-$249,999 range averaged 5.4. Lee County’s June numbers show expanding inventory alongside strong buyer engagement.

Robeson County

Robeson County continued to show year-over-year momentum, recording 370 showings in June, up 20.9 percent from last year. Buyer interest increased 33.4 percent to 2.1 showings per listing, while managed listings declined 9.4 percent to 213.

The $150,000-to-$249,999 range generated the most activity with 145 showings, followed by the $250,000-to-$349,999 range with 102. Homes priced at $350,000 and above recorded 62 showings, a substantial increase from the prior year. Robeson’s data points to growing buyer engagement across several price ranges, even as activity declined from May.

Looking Ahead

June’s housing data shows a region with greater inventory, positive pending and closed-sales activity, and continued price resilience. Buyers have more options, but desirable and well-positioned properties are still attracting meaningful attention. Sellers, meanwhile, should be prepared for longer marketing timelines and increased competition from both existing homes and new construction.

The market is not moving uniformly. Demand remains especially strong in certain attainable price ranges, while higher-priced inventory is growing and generally taking longer to sell. County-level showing activity also varies considerably, underscoring the importance of local knowledge.

For buyers and sellers alike, this remains a market where local expertise matters. Conditions continue to vary by county, by price point, and by property type, making hyper-local guidance more important than ever. For the most accurate neighborhood-level insight, Longleaf Pine REALTORS® members have the real-time market knowledge and professional expertise to help clients navigate today’s housing market with confidence.

You can find all the reports that produced this article here: